If you’ve ever wondered whether all the buzz around crypto is justified, you’re in the right place. I’ve spent years testing wallets, moving value across borders, and advising startups on digital payments. Here’s the bottom line: why is cryptocurrency better than traditional currency?

In key scenarios—speed, cost, transparency, accessibility, and ownership—crypto delivers advantages that are hard to ignore. This guide breaks down how, where, and why those advantages show up in real life, without hype and with practical examples you can apply today.

Source: www.slideteam.net

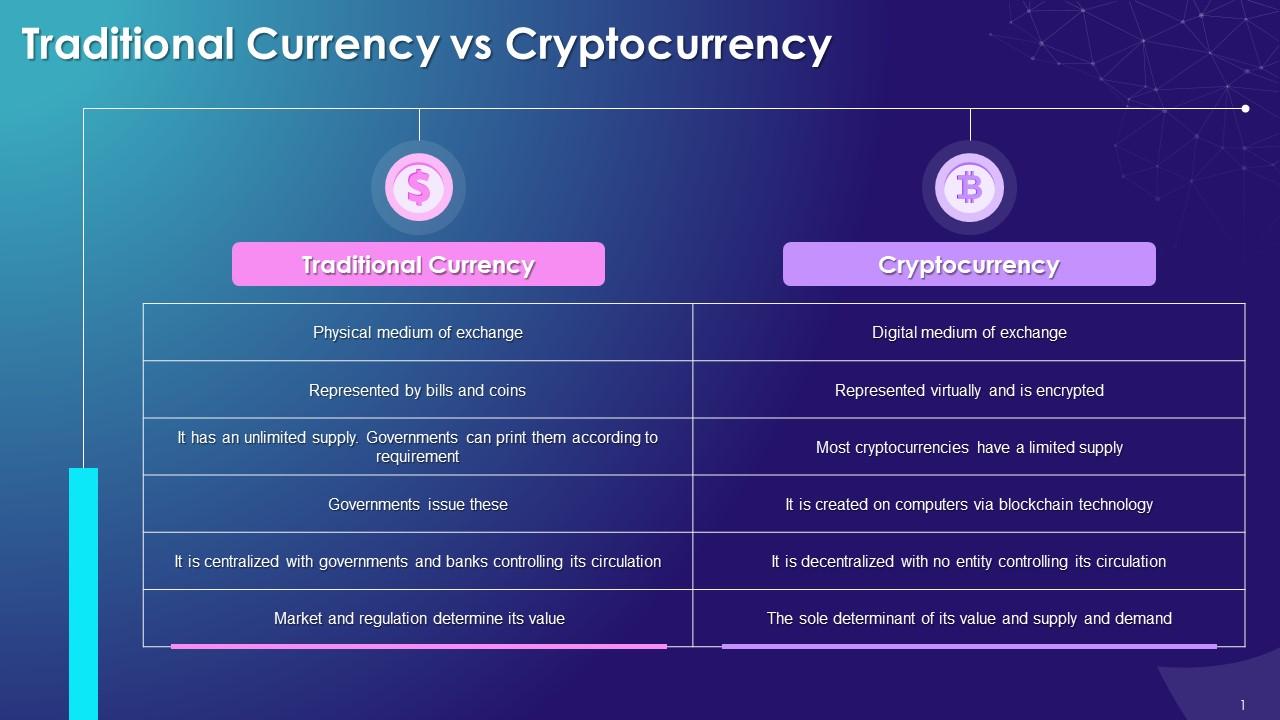

What Makes Crypto Different From Traditional Money

Let’s level-set. Traditional currency is centralized. Banks and governments manage issuance, settlement, and access. Crypto is built on decentralized networks that process and record transactions publicly and securely, usually without a single authority controlling the ledger.

Here’s the practical difference you’ll feel:

- Global by default. You can send value worldwide as easily as sending an email, often in minutes.

- Open 24/7. No bank hours, no settlement delays, no holidays.

- Self-custody option. You can hold and move assets without an intermediary.

- Programmable. Smart contracts let money follow rules automatically, from escrow to revenue sharing.

A helpful analogy: think of traditional currency like sending a letter by post—reliable, but slow, with multiple checkpoints. Crypto is more like instant messaging—peer to peer, time-stamped, and verifiable.

Source: www.travala.com

Speed, Access, And Borderless Payments

Cross-border transfers in fiat can take days and cost a lot in correspondent fees. With crypto, settlement can happen in seconds to minutes, depending on the network.

Real-world example from my work: I helped a freelancer in the Philippines get paid by a client in Canada. Bank wire quotes ranged from 3 to 5 days with $25 to $45 in fees. Using stablecoins on a low-fee chain, the payment arrived in under a minute and cost less than a dollar. The freelancer then used a local exchange to convert to pesos at competitive rates.

Where crypto shines for access:

- Unbanked and underbanked. If you can download a wallet, you can receive funds. No credit checks, no branch visits.

- Remittances. Families can avoid layers of intermediaries and opaque exchange rate markups.

- Emergency funds. During outages or local banking restrictions, crypto wallets still operate if you have connectivity and keys.

Tip: For predictable payments, consider stablecoins pegged to major currencies; they reduce price volatility while keeping crypto’s speed.

Source: www.currencytransfer.com

Security, Transparency, And Ownership

Blockchains are designed to be tamper-evident and auditable. Every transaction is recorded on a public ledger, which reduces the risk of hidden changes or off-the-books transfers.

What you actually get:

- Transparent ledgers. Anyone can verify a transaction’s status and history.

- Strong security model. Cryptography and decentralized consensus protect the network from single points of failure.

- True ownership. With self-custody, you control your private keys, not a bank. No freezes or chargebacks without your consent.

Personal insight: After a bank error locked my business account for 48 hours, I started keeping a portion of operational funds in a self-custodied wallet. When a client payment was due, I could still meet commitments without waiting for a human override. That redundancy reduced real business risk.

Caveat: Self-custody shifts responsibility to you. Use hardware wallets, store seed phrases offline, and enable multi-factor protections where possible.

Source: bullperks.com

Costs, Fees, And Middlemen

Traditional finance stacks fees: wire charges, intermediary banks, FX spreads, card interchange, chargeback risk premiums. Crypto can compress that stack.

Where costs often drop:

- Peer-to-peer transfers. Low fees on efficient networks, even for global payments.

- Merchant acceptance. Crypto payments can reduce card fees and eliminate chargebacks.

- Micropayments. Crypto enables small, frequent payments that are impractical with card rails.

Numbers to know: On some modern chains, average fees range from fractions of a cent to a few cents. For high-throughput use, scaling solutions and Layer 2s significantly reduce costs versus Layer 1 mainnets.

Transparency tip: Always check network congestion and fee estimators before sending, and choose the chain that matches your cost-speed needs.

Source: www.diversetechgeek.com

Inflation Resistance And Programmable Money

Many cryptocurrencies have fixed or predictable supply schedules, which can appeal in high-inflation environments. While not all crypto assets are deflationary, their issuance is typically known and transparent.

Two big differentiators:

- Monetary policy visibility. Issuance rules are encoded and auditable. You can model supply curves years ahead.

- Programmability. Smart contracts can automate financial logic: vesting schedules, streaming payments, decentralized lending, or escrow without a middleman.

A useful comparison: Traditional currency is like a closed device—you use what’s built in. Crypto is an open platform—you can install new “apps” for money. That’s why we see innovations like automated market makers, tokenized real-world assets, and community-governed treasuries.

Balanced perspective: Crypto is not a magic hedge. Asset prices are volatile. Stablecoins can mitigate volatility but carry counterparty or collateral risks. Due diligence is essential.

Source: blog.bitazza.com

Real-World Use Cases And Personal Lessons

From my experience implementing crypto payments for small teams and creators, here’s what worked and what didn’t:

What worked:

- Paying global contributors. Stablecoins + low-fee chains cut costs by 60 to 80 percent and reduced settlement time from days to minutes.

- Treasury diversification. Holding a small crypto allocation provided liquidity options during bank maintenance windows.

- Programmable workflows. Milestone-based payouts via smart contracts reduced disputes and admin work.

What to avoid:

- Ignoring compliance. Even with crypto, you still need KYC/AML processes when converting to fiat or paying contractors.

- Using the wrong chain at peak congestion. Fees can spike. Choose networks with predictable costs.

- Poor key management. Lost keys equal lost funds. Train your team on wallet hygiene and recovery procedures.

Starter checklist:

- Define your use case: savings, payments, remittances, or DeFi.

- Choose an appropriate asset: volatile crypto for growth, stablecoins for payments.

- Pick a reputable wallet and enable security features.

- Test with small amounts before scaling.

- Plan fiat on/off-ramps that comply with your local rules.

Risks, Limitations, And When Fiat Still Wins

Being realistic builds trust. Crypto isn’t better at everything.

Where fiat still leads:

- Price stability. Day-to-day budgeting works better in stable fiat units unless you use stablecoins.

- Consumer protections. Credit cards offer chargebacks and fraud protections that self-custody does not.

- Universal acceptance. Salaries, rents, and taxes usually require fiat.

Key risks to manage:

- Volatility. Use stablecoins for payments and set clear treasury policies for exposure.

- Custody errors. Invest in hardware wallets, multisignature, and secure backups.

- Regulatory shifts. Stay updated on local laws for reporting, taxes, and business usage.

- Counterparty risk. Centralized exchanges and custodians can fail; diversify and prefer reputable providers.

Evidence-based note: Industry data shows crypto usage surges in regions with high inflation, capital controls, or costly remittances, while mature markets adopt gradually through stablecoins and tokenized assets for efficiency. That pattern supports a practical takeaway: crypto is most “better” where traditional rails are slow, expensive, or restricted.

Frequently Asked Questions of why is cryptocurrency better than traditional currency

Is cryptocurrency really faster than bank transfers?

Yes, on most modern networks, crypto settles in minutes or less, 24/7. International bank transfers often take 1 to 5 business days. Speed varies by chain and network congestion.

How does crypto reduce fees compared to traditional payments?

Crypto can remove intermediaries and card networks, lowering per-transaction costs. On efficient chains, fees can be cents or less. Always compare network fees and exchange spreads before sending.

What about security—can my funds be stolen?

Crypto networks are secured by cryptography and decentralized consensus, but user security is crucial. Use hardware wallets, protect your seed phrase offline, and enable strong authentication. Most losses come from phishing or poor key management, not protocol failures.

Is crypto better for people without bank accounts?

Often, yes. Anyone with a smartphone can receive crypto, which helps unbanked users access payments and savings. Converting to local currency may still require a compliant on-ramp or peer-to-peer marketplace.

How do I avoid volatility if I want to use crypto for payments?

Use reputable stablecoins pegged to major currencies and transact on low-fee chains. Convert in and out quickly to minimize price exposure, and verify issuer transparency and reserves.

Can I use crypto legally in my country?

Regulations vary. Many countries allow crypto ownership and impose tax and reporting rules. Check local guidance, use compliant exchanges, and maintain good records for taxes.

Is cryptocurrency environmentally friendly?

It depends on the network. Many leading chains now use energy-efficient proof-of-stake, which dramatically reduces energy usage compared to older proof-of-work models.

Conclusion

Crypto isn’t here to replace traditional currency overnight—but it already outperforms in specific, high-impact areas: fast global transfers, lower fees, 24/7 access, transparent ownership, and programmable finance. If you’re a freelancer, a small business, a global team, or supporting family abroad, a practical crypto toolkit can save time and money while giving you more control.

Try this: set up a reputable wallet, send a small stablecoin transfer on a low-fee network, and compare the experience to a traditional wire. Document the costs, speed, and steps. Then decide where crypto fits your life or business.

Want more practical guides and real-world experiments? Subscribe, leave a comment with your use case, or share what’s worked for you.